The much-vaunted Special Relationship between Britain and the United States hasn’t always been so special. Leaving aside the American Revolutionary War and the War of 1812, economic and political relations between the world’s two leading Anglo powers have often been tumultuous. In the second half of the 19th century, for example, American protectionism clashed head-on with Britain’s free trade commitments. Tensions over the Irish question plagued relations between Britain and America well into the 1920s.

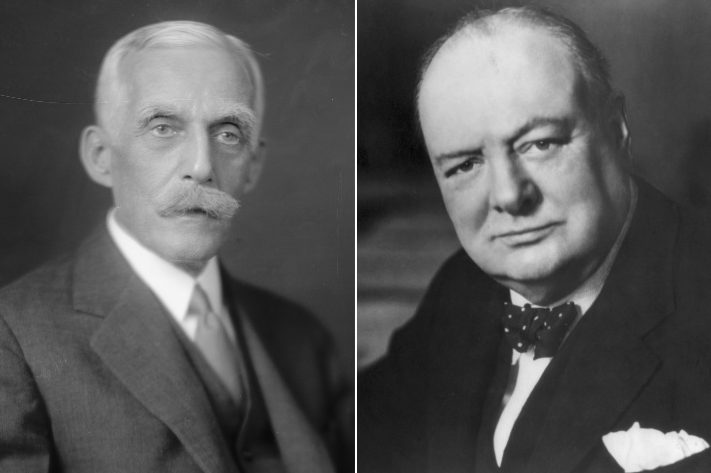

Winston Churchill may have had an American mother, but he was never inclined to think that British and American interests would always be aligned. Some of those differences revolved around economic questions, and at no time was Churchill more at odds with the United States than during his term as Britain’s chancellor of the Exchequer from 1924 until 1929. At the heart of the conflict was the vexed issue of the huge postwar debts owed by European nations to each other and, above all, to the United States. Churchill’s quest to reduce the U.K.’s debts to America brought him into conflict with Andrew Mellon, the 49th secretary of the Treasury under presidents Warren Harding, Calvin Coolidge, and Herbert Hoover between 1921 and 1932.

Mellon is far less known than Churchill and has received less attention from historians than many Treasury secretaries whose term of office was shorter and less consequential. Mellon’s importance, however, for American economic history and relations is central to Jill Eicher’s new book, Mellon vs. Churchill: The Untold Story of Treasury Titans at War, in which she shows how profound policy differences about debt and public finances put Britain and America severely at odds for a tense decade.

A former investment banker who spent time as a Treasury Department official before entering the academic world, Eicher’s background serves her well in understanding the financial and institutional dynamics that characterized economic relations between Britain and America in the 1920s. After 1918, successive British governments sought to tackle the economic problems bequeathed to it by World War I while maintaining London’s status as a financial superpower.

America, however, was determined to collect the bills for the massive loans it had made to help fund the Allied war effort long before it formally entered the conflict in 1917. Further complicating matters was an acute awareness on the part of leaders of both nations that the United States was now the undisputed big kid on the geopolitical block and that Britain did not bestride the world quite as much as it did before 1914.

Much of the economic conflict and subterranean geopolitical tensions were fought out, Eicher shows, between the loud and immensely self-confident Churchill and the quieter, more reserved Mellon. Both men understood what was at stake financially, politically, and in terms of prestige.

Neither Churchill nor Mellon adopted extreme positions on the issue of debt repayments. Churchill was perfectly aware that expecting America simply to forgive the entire debt was a seriously bad idea, not least because it would undermine Britain’s long-term credit. Mellon likewise understood how the debt burdens incurred by European states during the war were impeding their ability to address the severe economic problems of the immediate postwar period. And overshadowing everything else, both men realized, was the political wrangling surrounding the explosive issue of German reparations.

In the case of America, Eicher shows that Mellon’s measured approach to debt repayment put him at odds with the majority of Americans who insisted on full repayment, because that is what Republican and Democrat politicians had promised the electorate. The Senate, she points out, was especially firm on this point, primarily because senators resented how the executive branch under Woodrow Wilson had intruded upon the Senate’s foreign policy prerogatives. Other Americans took another view. Many Wall Street bankers and some scholars were worried that too firm a position on the debt issue could severely damage America’s relationship with Britain, its global empire, and the rest of Western Europe.

Mellon walked a fine line between these groups. He affirmed the principle that freely incurred debts should be paid. Yet he also recognized that an insolvent Europe would diminish the ability of American businesses to sell their wares in European markets. Churchill, however, insisted on drawing contrasts between what he regarded as Britain’s generous approach to the debts that it was owed by France and Italy, with what he portrayed as American greed. Mellon was left displeased and with the sense that Churchill did not understand the relative leniency of America’s position, given the immense domestic pressures on the U.S. government to make Britain pay up.

Much of the book tracks the back-and-forth between the two men and how they kept being drawn into conflict, despite often holding similar views. Eicher’s account, however, also stresses how these arguments were played out in public through the press. What had once been a realm of policy dominated by government financial officials and major banking firms and relatively shielded from public view swiftly became subject to intense scrutiny by American and British newspapers.

It did not consequently take long for vitriol and selective outrage to become the name of the game. Tensions between Mellon and Churchill were further exacerbated by the tone of high indignation that increasingly marked press commentary in both countries concerning Washington and London’s differences. Indeed, Churchill did not hesitate to use newspapers to press his case, whether through what we would call “leaks” or via opinion pieces that he penned himself—a practice deplored by some of his cabinet colleagues. Mellon, conversely, was more inclined to exert pressure the old-fashioned way, such as through dinners for government officials during which subtle but serious strong-arming would occur.

Eicher makes a point of showing how the debt fight between Mellon and Churchill spilled over to other areas of economic policy: most notably, tariffs. For example, American business and political leaders called for a reduction in intra-European tariff barriers as well as reducing European tariffs on American goods so as to accelerate the process of economic readjustment. This, it was argued, would make it easier for European nations to pay their debts to each other and America. Not surprisingly, Europeans responded by noting that the United States had high tariff barriers, and it was only fair that Washington do for itself what it was demanding of others.

The Mellon-Churchill clash wound down at the end of the 1920s, especially after Churchill exited the British cabinet following the 1929 general election. Needing to make some money, Churchill engaged in an extensive book-promotion tour across the United States. “In virtually every speech,” Eicher notes, Churchill “called for Anglo-American cooperation and friendship”—something, she states, that he “did not extend to Mellon.”

Not long afterwards, the rickety structures put in place to manage debt repayments and reparations in the 1920s collapsed as the 1929 stock market crash exposed the degree to which German and Austrian businesses and banks were dependent on American loans. This helped trigger the chain of events that would eventually lay low the Weimar Republic and plunge the world into a protracted depression.

Neither Churchill nor Mellon, however, appear to have indulged in mutual rancor after these events. In fact, Eicher ends her tale with Churchill and Mellon sitting next to each other at a dinner in London on July 12, 1932, to mark the bicentennial of George Washington’s birth. Mellon was present because he had taken up the post of U.S. ambassador to the Court of St. James only three months earlier.

Churchill, Eicher reports, made a speech in which he praised America’s first president and celebrated the longstanding relationship between the two Anglo powers. Churchill did, however, reference “competing commercial interests” and stressed that there were bound to be “some tiresome arguments about money matters.”

The remarks were made in good humor and were received as such by those in attendance. One cannot help wondering, however, if Churchill was underscoring something that Mellon, with his long involvement in business and politics, surely knew: that commercial and economic disputes can rupture the closest of cultural and historical relationships because the former ultimately trump the latter in great power politics. That is sound advice to reflect upon in our own time.

Mellon vs. Churchill: The Untold Story of Treasury Titans at War

by Jill Eicher

Pegasus Books, 368 pp., $32

Samuel Gregg is Friedrich Hayek Chair in Economics and Economic History at the American Institute for Economic Research. His most recent book is The Next American Economy: Nation, State, and Markets in an Uncertain World (2022), and he can be followed on X @drsamuelgregg.

Original News Source – Washington Free Beacon

Running For Office? Conservative Campaign Management – Election Day Strategies!